Companies must have a suitable chart of accounts and there are no provisions as to the contents and structure of a chart of accounts.

Only an outline provision stating that a company must have a chart of accounts designed for its individual requirements. This means that you are allowed to design your own account numbering.

The purpose of a chart of accounts is to secure a fixed structuring of the accounts created in the bookkeeping, used also for the treasury management.

Typically, the chart is structured like this:

- accounts concerning the day-to-day running of the company, shows the company’s earnings and expenses (profit and loss)

- asset accounts, shows the values in the company (assets)

- liability accounts, shows the debt/financing of the company (liabilities)

The program makes a standardized chart of accounts available; therefore, you just need to adjust it to suit your company’s specific requirements.

When you make an account plan for your company you need to know which activities you want to have information about. The shortest account plan you can make consists of two accounts:

000001 Income

000002 Expenses

If you only have these two accounts for registering information about your company’s economy, you will not be able to find out which activities are working well or badly. The only thing you can see is if the company in general is losing or making money. This is too little information for a modern project or company.

Consider carefully what information you need from your new business. The information you need should be shown in the account plan.

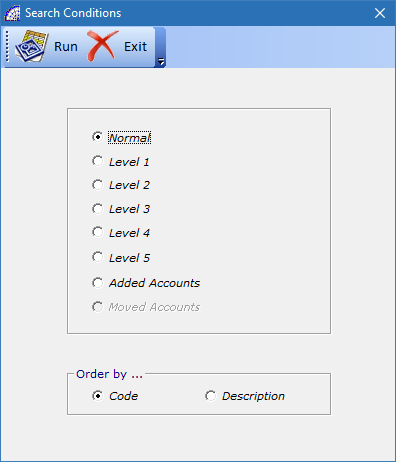

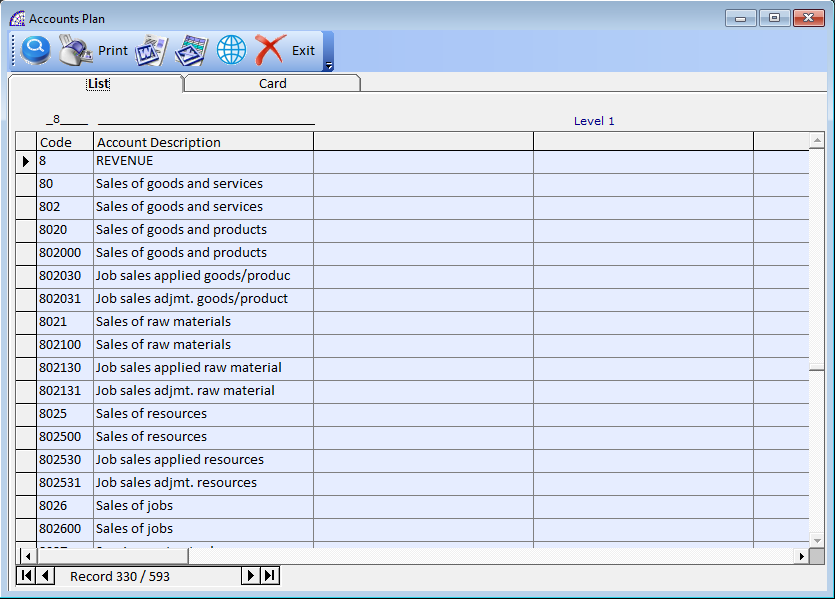

Each account has, besides its name, its own number. It makes it easier to work with in the daily tasks with the accounting or treasury data.![]() The program offers ten main levels, that you can look at pressing the relative command and selecting the “Level 1” option in the search conditions:

The program offers ten main levels, that you can look at pressing the relative command and selecting the “Level 1” option in the search conditions: